{kind=link}

© 2025 DiscoverTheState.com. All rights reserved. Powered by DiscoverTheState.com

Washington Housing Slump 2025 – 10 Cities Quietly Entering Freefall

Intro: why this market matters now

The Washington housing slump 2025 isn’t loud. It’s behavioural. Open houses feel emptier. Listings reappear. “Price improvement” becomes the default language.

Meanwhile, the state still has the same assets: ports, aerospace, government jobs, healthcare, and a tech spine. However, the cost to carry a home has changed faster than household budgets. As a result, momentum breaks before headlines show up.

If you want a regional comparison, the same “quiet correction” pattern is showing up next door in Oregon too: Oregon’s Housing Market Slumps — These Cities Are Facing a Price Correction. Discover The Estate

Key warning signals in the Washington housing slump 2025

This isn’t about vibes. It’s about repeatable signals that show up before a “crash” label ever appears.

Here’s what to watch, city by city:

-

Days on market rising: Homes that used to vanish after one weekend now sit through multiple.

-

List-to-sale ratios slipping: More deals close at or under ask, not above.

-

Multiple price cuts: Two and three reductions on the same address becomes normal.

-

Concessions returning: Seller credits, repair credits, and rate buydowns come back as tools.

-

Fall-throughs increasing: Inspection, appraisal, and financing kill more contracts.

To keep yourself honest, anchor your “feel” to real dashboards:

-

Redfin Data Center: https://www.redfin.com/news/data-center/ redfin.com

-

Zillow research data: https://www.zillow.com/research/data/ Zillow

-

Mortgage rate baseline (FRED): https://fred.stlouisfed.org/series/MORTGAGE30US FRED

And zoom out. When the West Coast reprices, it rarely stays isolated. These comparisons help:

-

California Housing Crash Update – 9 Cities Where Prices Just Broke in 2025 Discover The Estate

-

Nevada Housing Meltdown – 10 Desert Cities Drowning in Price Cuts Discover The Estate

-

U S Suburbs Turning Into Housing Ghost Towns in 2025 Discover The Estate

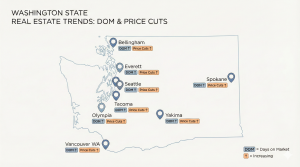

The 10-city breakdown: where the shift shows up first

This is a countdown from “mild warning signs” to “flagship wobble.”

#10 Bellingham

Bellingham still sells a lifestyle story: college town, border proximity, water views, and mountain access. However, the buyer pool is budget-limited.

Watch for:

-

View-adjacent homes sitting longer

-

Sellers leaning on small cuts instead of one big reset

-

STR expectations quietly unwinding

#9 Yakima

Yakima looks “affordable” on sticker price. The problem is operating cost and condition risk.

Watch for:

-

Tough inspections on older roofs and systems

-

Insurance and utilities turning “cheap” into “heavy”

-

Investors underwriting harder and walking more often

#8 Puyallup and South Pierce belts

The pitch was “more house for the money.” The reality is commute cost plus a higher mortgage.

Watch for:

-

Concessions becoming normal

-

Builders pushing buydowns

-

Resales chasing the market down in small steps

#7 Vancouver, Washington

Vancouver rode the Portland-adjacent narrative for years. When demand cools, sameness becomes a liability.

Watch for:

-

Identical subdivision listings stacking reductions

-

Buyers negotiating like it’s a business deal

-

“Move-in ready” outperforming anything dated

#6 Olympia–Lacey–Tumwater

Government-town stability helps. Still, fixed incomes hit limits when taxes, insurance, and HOA costs rise together.

Watch for:

-

First cuts showing up earlier in the listing cycle

-

HOA communities feeling more sensitive to dues

-

Buyers refusing “future projects” unless priced correctly

#5 Everett and Snohomish County belts

Commuter math is brutal when rates are high. A long drive plus higher carrying costs changes demand.

Watch for:

-

Builders advertising rate buydowns and credits

-

Buyers getting picky on layout, condition, and schools

-

Listings lingering after the first weekend

#4 Spokane

Spokane became a remote-work darling. That trade breaks when demand softens and supply builds.

Watch for:

-

Newer subdivision inventory needing incentives

-

Investor-heavy pockets getting hit first

-

Price cuts spreading from fringe areas inward

#3 Tacoma

Tacoma was the “budget Seattle” narrative. In a slump, buyers underwrite everything.

Watch for:

-

More inspection and appraisal friction

-

Listings anchored to 2021 comps sliding in stages

-

Buyers demanding credits for roof, sewer, and major systems

#2 Seattle non-prime belts

Not every Seattle segment behaves the same. In 2025, anything that isn’t truly A-plus has to negotiate.

Watch for:

-

Condo/townhome segments requiring incentives

-

Buyers asking about HOA reserves and assessments early

-

“Brand-only” pricing failing without fundamentals

Use FEMA flood mapping as a risk sanity-check in water-adjacent areas (insurance and risk pricing matter more in this phase): https://msc.fema.gov/portal/home msc.fema.gov

#1 Bellevue and the Eastside

The flagship story is quality schools, tech wealth, and “you can’t overpay.” In a payment-driven market, even flagships wobble.

Watch for:

-

Jumbo loan sensitivity (payment shock is real)

-

Inventory thickening in specific condo/townhome bands

-

Awkward reductions replacing bidding wars

What this means for buyers

Your advantage isn’t speed. It’s structure.

-

Build a watchlist of stale inventory (21–45+ days), especially after a second cut.

-

Treat list price as an opening position, not a command.

-

Keep contingencies: inspection and financing are leverage now.

-

Negotiate with line items: repairs, credits, and permanent rate buydowns.

-

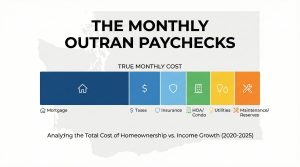

Run a five-year monthly: mortgage + taxes + insurance + HOA/dues + utilities + reserves vs comparable rent.

If the deal only works after financial gymnastics, it doesn’t work. Meanwhile, walking away is a skill, not a failure.

What this means for sellers

The market isn’t out to get you. It will, however, punish denial.

-

Price to pendings and closings today, not peak screenshots.

-

Do a pre-inspection to control surprises and reduce renegotiations.

-

Lead with incentives (credit, buydown, repair plan) instead of bleeding with micro-cuts.

-

Make the house easy to trust: clean disclosures, service records, and a realistic repair posture.

In addition, be honest about the segment you’re in. A-plus homes still move. “Normal” homes need terms.

What this means for investors

Washington 2025 is a stress test. Treat it like one.

-

Appreciation is not Plan A. Cash flow and reserves are.

-

Underwrite taxes, insurance, HOA/condo dues, maintenance, vacancy, and capex conservatively.

-

In condo markets, be obsessive about HOA reserves and special assessment risk.

-

“Safe” now means the asset pays you to hold it even if prices nap for years.

For macro grounding, track the FHFA HPI (broad pricing trend context): https://www.fhfa.gov/data/hpi/ FHFA.gov

Final takeaways

Washington isn’t “over.” It’s being repriced so payments and paychecks can exist in the same universe again.

If you’re buying, operate like a calm negotiator with a spreadsheet.

If you’re selling, price like it’s 2025 and offer terms like a pro.

If you’re investing, demand cash flow and treat hype as noise.

This article is educational and not financial, legal, or tax advice. Always verify local data and consult licensed professionals.

Watch the full video breakdown on our Discover the State YouTube channel.

FAQ

Is the Washington housing slump 2025 a crash or a reset?

For most cities, it looks like a reset first: longer days on market, more cuts, and more concessions. A “crash” is usually later-stage behaviour, not the opening chapter.

What are the earliest signs of the Washington housing slump 2025 in my ZIP?

Look for repeat reductions, rising days on market, and listings that keep coming back after pending. Also track whether seller credits are becoming common in your neighbourhood.

Is it a good time to buy in Washington in 2025?

It can be—if you’re buying the monthly, not the story. Run the five-year monthly, keep contingencies, and negotiate credits or buydowns when listings go stale.

How should sellers price during the Washington housing slump 2025?

Price to what’s closing now, not to 2021–2022 comps. If you’re not getting traction in 10–14 days, your price or terms are off versus the segment.

What data should I watch weekly in Washington right now?

Start with days on market, price cuts, list-to-sale ratios, and inventory. Redfin and Zillow dashboards help, and mortgage rate trends set the affordability ceiling. (Links above.)

No Comments